The organization is on sleep. Ip income minus expenses on a simplified basis. Tax and reporting periods on the simplified tax system

Methods of accounting for accepted income in 2019 on a simplified basis

The simplified person needs to take into account income in order to comply with 2 goals:

- calculating the tax base, advances and tax payable at the end of the year;

- control of the income limit - in 2019, the simplified taxation system of 6 percent can be applied if the income does not exceed 150 million rubles. in a year.

For the correct calculation of the tax under the simplified tax system, "income" will need to study the general procedure for recognizing income and expenses for simplified taxpayers, which is set out in Art. 346.17 of the Tax Code of the Russian Federation. Revenues are subject to taxation and are recognized as income on a cash basis:

- as of the date of receipt of funds to the bank account;

- the date the cash was deposited into the taxpayer's cash desk;

- the day of obtaining property rights, other property, debt repayment;

- the date of payment of the bill.

Income is divided into income from operating activities and non-operating income.

Everything that is income with a simplified taxation system of 6% is set out in more detail in Art. 249 of the Tax Code of the Russian Federation:

|

The main type of activity on a simplified basis of 6 percent |

Revenues recognized for taxation |

|

Trade |

Receipts from the sale of purchased goods, repayment of accounts receivable, prepayment for the supply of goods |

|

Payments for work: construction, installation, transport, information, repair and other services provided |

|

|

Production |

Calculations for the sale of own products |

|

Intermediary activity |

Commission (letter of the Ministry of Finance of the Russian Federation dated 04.09.2013 No. 03-11-06 / 2/36404) |

|

Separate ways to generate income |

Proceeds from the sale of property or rights to this property, income associated with a long stage of production, as well as other income provided for in Art. 271 and 273 of the Tax Code of the Russian Federation |

Receipts can be both in monetary terms and in kind.

Don't know your rights?

What non-operating income to accept at a tax rate of 6%

The simplified taxpayers refer to the number of non-operating incomes (Article 250 of the Tax Code of the Russian Federation):

- income from participation in a simple partnership;

- surpluses revealed during the inventory;

- gratuitous receipt of property or property rights;

- amounts received as a result of revaluation of foreign exchange funds (in terms of positive difference);

- the amount of interest under loan agreements, credit, bank deposit as well as for securities;

- written off accounts payable;

- proceeds from the transfer of real estate, land plots for use under lease / sublease agreements - in this case, income can be not only the amounts of lease payments themselves, but also, for example, inseparable improvements to the leased property that were made without agreement with the lessor (letter of the Ministry of Finance dated 09.09.2013 No. 03-11 -06/2/36986);

- compensated losses, penalties, fines for violation of contractual relations, in case of recognition as a debtor or by a court decision (letter of the Ministry of Finance dated 01.07.2013 No. 03-11-06 / 2/24984);

- profit from participation in other organizations.

Non-operating income is subject to mandatory accounting when calculating the tax base of the USN "income" and fixing it in the KUDiR.

For organizations that decide to use the 6% simplification, the legislation provides for cases when income is not taxed.

What income should not be taken into account when calculating the tax base

There are a number of operations that do not fall into the base when calculating the tax rate of STS-income. These include, in particular, the following receipts (Article 251 of the Tax Code of the Russian Federation):

- as reimbursement of expenses for insured events from the FSS;

- from counterparties for the formation of a pledge, a deposit;

- from other payers for the creation of charter / share capital;

- net assets of property for the formation of additional capital;

- from agents, commission agents (financial assets or property) in the framework of intermediary contracts;

- from borrowers under credit agreements, loan agreements (except for cases of payment of interest).

Information about these transactions is collected separately in the respective accounting accounts.

Cash method of accounting for income under a simplified taxation system: nuances

On a simplified income taxation system, it is important to determine the moment of income recognition. If income is expressed in monetary form, then the fact of their receipt is established in accordance with the date of receipt of money in the cashier's office or on the current account. The supporting document in this case is PKO, cashier's check, bank statement. Based on these documents, entries are formed in the book of income and expenses of organizations and individual entrepreneurs on the simplified tax system (KUDiR, approved by order of the Ministry of Finance of the Russian Federation of October 22, 2012 No. 135n).

If the calculations are carried out in a non-monetary form, then the date of recognition of income is the day of receipt of property or property rights, or the day of repayment of the debt in another way. For documentary confirmation of the receipt of assets or property rights, an act of acceptance and transfer can be drawn up, on the date of which the income is reflected in the KUDiR.

In the case of mutual settlements, the date of recognition of income is the day of signing the act of mutual settlements of the company. Such nuances are specified by the letter of the Ministry of Finance dated 10.24.2012 No. 03-11-06 / 2/135.

Advances received to the current account or to the cash desk of the company, according to the rules of the cash basis, are recognized as income on the day of their actual enrollment, regardless of the fact of the performance of work or the shipment of products, on account of which the advance was received (subparagraph 1 of clause 1 of article 251, Clause 2 of Article 273 of the Tax Code of the Russian Federation).

If an organization makes settlements with customers using an electronic payment system (electronic money), the date of recognition of income on a simplified system is the moment when the operator debits the money from the buyer's account and credits it to the seller's electronic account. An important detail such an operation consists in the fact that the order to write off funds from the buyer's account and credited to the counterparty's account must be carried out simultaneously. Such a rule is established by clause 10 of Art. 7 of the Law "On the National Payment System" dated June 27, 2011 No. 161-FZ.

On the simplified tax system, the company can choose one of the objects of taxation: income or income reduced by the amount of expenses. If a simplified income system is chosen, then the company should carefully analyze its receipts so as not to include tax-exempt funds in the tax base.

The single tax under the simplified tax system is paid by companies and entrepreneurs who voluntarily switched to the “simplified tax system”. For the object of taxation "income" the rate is 6%. For the object of taxation "income minus expenses" the rate is 15%. This material, which is part of the "Tax Code" for Dummies "cycle, is dedicated to Chapter 26.2 of the Tax Code of the Russian Federation" Simplified taxation system ". This article is available, in simple language, tells about the procedure for calculating and paying a single "simplified" tax, about the objects of taxation and tax rates, as well as the timing of reporting. Please note: The articles in this series only provide a general overview of taxes; for practical activities it is necessary to refer to the primary source - Tax Code Russian Federation

Who can apply the simplified tax system

Russian organizations and individual entrepreneurs who voluntarily chose the simplified tax system and who have the right to apply this system... Companies and entrepreneurs who have not expressed a desire to switch to the "simplified" system, by default, apply other taxation systems. In other words, the transition to the payment of a single “simplified” tax cannot be compulsory.

Fill out and submit a notification of the transition to the simplified tax system via the Internet

What taxes do not need to be paid when applying the simplified tax system

In general, organizations that have switched to the "simplified" system are also exempt from property tax. Individual entrepreneurs - from personal income tax and property tax of individuals. In addition, both do not pay value added tax (except for VAT on imports). Other taxes and fees must be paid in accordance with the general procedure. So, "simplified" must make payments for compulsory insurance from the salaries of employees, withhold and transfer personal income tax, etc.

However, from general rules there are exceptions. So, from January 1, 2015, some "simplified" have to pay property tax. From that date, the exemption from the payment of this tax does not apply to real estate objects in respect of which the property tax base is determined as the cadastral value. This property includes, for example, retail and office real estate (clause 1 of Art. Tax Code of the Russian Federation, clause 3 of Art. Tax Code of the Russian Federation).

Where the simplified system operates

Throughout the Russian Federation without any regional or local restrictions. The rules for switching to the simplified tax system and returning to other taxation systems are the same for all Russian organizations and entrepreneurs, regardless of location.

Who is not entitled to switch to the simplified tax system

Organizations that have opened branches, banks, insurers, budgetary institutions, pawnshops, investment and non-state pension funds, microfinance organizations, as well as a number of other companies.

In addition, “simplified” is prohibited for companies and entrepreneurs that produce excisable goods, extract and sell minerals, work in the gambling business, or have switched to paying a single agricultural tax.

Restrictions on the number of employees, the value of fixed assets and the share in the authorized capital

It is not entitled to switch to a simplified system of organization and individual entrepreneurship if the average number of employees exceeds 100 people. The transfer ban also applies to companies and entrepreneurs with a residual value of fixed assets of more than 150 million rubles.

In addition, in the general case, STS cannot be applied to enterprises if the share of participation in them by others legal entities more than 25%.

How to switch to the simplified tax system

Organizations that do not belong to the above categories can switch to the simplified tax system if their income for the period from January to September did not exceed 112.5 million rubles. If this condition is met, you must submit a notification to the tax office no later than December 31, and from January next year, you can apply the "simplified tax". After 2019, the specified limit must be multiplied by the deflator coefficient. For 2020, the value of the coefficient is 1. This means that the marginal amount of income in 2020 remained at the same level.

Entrepreneurs who do not belong to the above categories can switch to the simplified tax system, regardless of the amount of income for the current year. To do this, they need to submit a notification to the tax office no later than December 31, and from January next year the individual entrepreneur will be able to apply the simplified taxation system.

Newly created enterprises and newly registered individual entrepreneurs have the right to apply a simplified system from the date of registration with the tax office. To do this, you must submit a notification no later than 30 calendar days from the date of tax registration.

Organizations and individual entrepreneurs who have ceased to be taxpayers of UTII can switch to a “simplified tax system” from the beginning of the month in which their obligation to pay a single “imputed” tax was terminated. To do this, you must submit a notification no later than 30 calendar days from the date of termination of the obligation to pay UTII.

Violation of the deadlines for filing an application for the application of the simplified tax system deprives a company or an entrepreneur of the right to use the simplified system.

How long do you need to apply the "simplified"

A taxpayer who switched to the simplified tax system must apply it until the end of the tax period, that is, until December 31 of the current year inclusive. Until that time, it is impossible to voluntarily abandon the STS. You can change the system of your own free will only from January 1 of the next year, about which you need to notify the tax office in writing.

An early transition from the simplified system is possible only in cases where a company or entrepreneur has lost the right to a “simplified system” within a year. Then the abandonment of this system is mandatory, that is, it does not depend on the desire of the taxpayer. This happens when revenues for a quarter, six months, nine months or a year exceed 150 million rubles (after 2019, the specified value must be multiplied by the deflator coefficient, in 2020 this coefficient is 1). Also, the right to the simplified tax system is lost when the criteria for the number of employees, the cost of fixed assets or the share in the authorized capital cease to be met. In addition, the right to “simplified” is lost if the organization falls into the “forbidden” category in the middle of the year (for example, opens a branch or starts producing excisable goods).

The termination of the application of the "simplified tax" occurs from the beginning of the quarter in which the right to it is lost. This means that an enterprise or individual entrepreneur, starting from the first day of such a quarter, must recalculate taxes using a different system. Penalties and fines in this case are not charged. In addition, if the right to a simplified system is lost, the taxpayer must notify the tax office in writing about the transition to a different taxation system within 15 calendar days after the end of the relevant period: a quarter, half a year, nine months or a year.

If the taxpayer has ceased to engage in activities in respect of which he applied the simplified system, then within 15 days he must notify his inspectorate.

Objects "USN income" and "USN income minus expenses". Tax rates

A taxpayer who switched to a simplified system must choose one of two objects of taxation. In fact, these are two ways of calculating a single tax. The first object is income. Those who chose it sum up their income for a certain period and multiply it by 6%. The resulting figure is the size of the single "simplified" tax. The second object of taxation is income reduced by the amount of expenses (“income minus expenses”). Here the tax is calculated as the difference between income and expenses multiplied by 15%.

The Tax Code of the Russian Federation gives the regions the right to establish a reduced tax rate depending on the category of the taxpayer. A rate reduction can be entered both for the “income” object and for the “income minus expenses” object. You can find out what preferential rates are accepted in your area by contacting your tax office.

You need to choose an object of taxation even before switching to the simplified tax system. Further, the selected object is applied throughout the entire calendar year. Then, starting from January 1 of the next year, you can change the object, having previously notified your tax office of this no later than December 31. Thus, you can move from one object to another no more often than once a year. There is an exception: the parties to a joint venture agreement or a property trust agreement are deprived of the right to choose, they can only use the “income minus expenses” object.

How to record income and expenses

Taxable income under the simplified tax system is the proceeds from the main activity (income from sales), as well as amounts received from other activities, for example, from the lease of property (non-operating income). The list of expenses is strictly limited. It includes all popular cost items, in particular, wages, the cost and repair of fixed assets, the purchase of goods for further sale, and so on. But at the same time, there is no such item in the list as "other expenses". Therefore, the tax authorities are strict during inspections and cancel any costs that are not directly mentioned in the list. All income and expenses should be recorded in a special book, the form of which is approved by the Ministry of Finance.

With a simplified system, it is used. In other words, income is generally recognized at the time the money is received on the current account or in the cashier's office, and expenses are recognized at the time when the organization or individual entrepreneur has paid off the obligation to the supplier.

Maintain tax and accounting records under the simplified tax system in an intuitive web service

How to calculate a single "simplified" tax

It is necessary to determine the tax base (that is, the amount of income, or the difference between income and expenses) and multiply it by the appropriate tax rate. The tax base is calculated on an accrual basis from the beginning of the tax period, which corresponds to one calendar year. In other words, the base is determined during the period from January 1 to December 31 of the current year, then the calculation of the tax base starts from zero.

Taxpayers who have chosen the object "income minus expenses" must compare the amount of the single tax received with the so-called minimum tax. The latter is equal to one percent of income. If single tax, calculated in the usual way, turned out to be less than the minimum, then the minimum tax must be transferred to the budget. In subsequent tax periods, the difference between the minimum and “regular” tax may be included in expenses. In addition, those for whom the object is "income minus expenses" can carry forward losses in the future.

When to transfer money to the budget

No later than the 25th day of the month following the reporting period (quarter, half year and nine months), you need to transfer the advance payment to the budget. It is equal to the tax base for the reporting period multiplied by the appropriate rate, minus advance payments for prior periods.

At the end of the tax period, it is necessary to transfer to the budget the total amount of the single "simplified" tax, and for organizations and entrepreneurs there are established different terms payment. So, enterprises must transfer money no later than March 31 of the next year, and individual entrepreneurs - no later than April 30 of the next year. When listing the total amount of tax, you should take into account all advance payments made during the year.

In addition, taxpayers who have chosen the “income” object reduce advance payments and the total amount of tax on mandatory pension and medical insurance contributions, contributions for compulsory insurance in case of temporary disability and in connection with maternity, for voluntary insurance in case of temporary disability of employees, and also for sick leave payments for employees. At the same time, the advance payment or the total tax amount cannot be reduced by more than 50%. In addition to this, from January 1, 2015, the possibility of reducing the tax by the full amount of the paid trade tax was introduced.

How to report under the simplified tax system

You need to report on the single "simplified" tax once a year. Companies must submit a declaration on the simplified taxation system no later than March 31, and entrepreneurs - no later than April 30 of the year following the expired tax period. Reporting for the quarter, six months and nine months is not provided.

Taxpayers who have lost the right to a "simplified tax" must submit a declaration no later than the 25th day of the next month.

Companies and individual entrepreneurs who have ceased to engage in activities falling under the “simplified” must submit a declaration no later than the 25th day of the next month.

Combining the simplified tax system with imputation or with the patent system

A taxpayer has the right to charge “imputed” tax for some types of activity, and a single tax under the simplified tax system for others. It is also possible that an entrepreneur applies a “simplified tax system” for some types of activity, and a patent taxation system for others.

In this case, it is necessary to keep separate records of income and expenses related to each of the special modes. If this is not possible, then the costs should be allocated in proportion to the income from activities subject to different tax systems.

One of the most popular tax regimes, especially among individual entrepreneurs, is the simplified system (simplified tax system or simplified tax system). Its main feature is that instead of income tax, VAT, property tax, a single tax is paid to replace them. At the same time, the tax burden is less than on OSNO, and accounting for individual entrepreneurs and LLCs is much easier, so it can be kept independently.

Organizations and entrepreneurs who want to apply the simplified tax system can choose two options for calculating taxes:

- The simplest one is the rate at which is 6%.

- More complex, but in some cases it is more profitable to use it - this is STS "income minus expenses", the rate is, depending on the availability of benefits, from 5 to 15%, but most often it is still 15%.

Terms of use of the simplified tax system

The use of the simplified version has some limitations, therefore, first of all, you need to understand whether your business does not fall under them (Tax Code of the Russian Federation, article 346.12, clause 3).

Number:

- This type of taxation can only be applied by small businesses, in which the number of hired employees does not exceed 100 people.

For what type of activity and what organizations and individual entrepreneurs cannot apply given view taxation:

- Insurers, banks, microfinance organizations, pawnshops, investment funds, pension funds of non-state education, securities market participants working on a professional basis.

- If an individual entrepreneur or LLC is engaged in the sale, extraction of minerals, the exception is common ones, for example, such as sand, crushed stone, peat.

- LLC and individual entrepreneur that are engaged in the production of excisable goods (gasoline, alcohol, tobacco products, etc.).

- Lawyers with a lawyer's office, notaries who are engaged in private practice, etc.

- Business entities applying.

- Organizations that participate in production sharing agreements.

- If the share of participation in the organization of other organizations is more than 25%, with the exception of non-profit organizations; educational and budgetary institutions; also organizations whose authorized capital consists of 100% of contributions made by public organizations of disabled people.

- In case of excess of 100 million rubles. residual value of fixed assets.

- The simplified taxation cannot be applied by foreign organizations.

- Budgetary and state institutions.

- If an organization or individual entrepreneur has submitted an application for the simplified tax system, required for the transition to this tax system, not within the time frame established by law.

- Organizations that have branches.

On January 1, 2016, amendments entered into force, according to which, upon fulfillment of the described conditions organizations have the right to apply the simplified tax system if they have their representative offices, for the branches everything remained unchanged.

By income:

- If the company's annual income exceeds certain turnovers, so in 2014 it was 60 million rubles, in 2015 the level was increased to 68.82 million rubles, in 2016 the limit is 79.74 million rubles. Therefore, under the same condition, if the company, based on the results of 9 months of its work, did not exceed the level of income of 45 million rubles, then it can switch to a simplified system from next year by submitting an application in the form 26.2-1.

Important! From January 1, 2017, the threshold value for the transition to the simplified tax system is increasing. At the end of 2016, income should not exceed 59 million 805 thousand rubles.

The procedure for switching to the simplified tax system

The transition to a simplified system, by submitting an application, can be carried out in the following terms:

- When organizing a company, along with documents for registration.

- Within 30 days after registration.

- Until December 31 of the year preceding the application of the simplified tax system.

- In order not to wait a whole year, you can close and immediately open the IP by submitting the necessary notification.

What to choose STS "Income" or "income minus expenses"?

In order to choose the type of taxation, you need to understand what is behind it. We will briefly describe each of them, you can read in more detail on our website in other articles.

In order to choose the type of taxation, you need to understand what is behind it. We will briefly describe each of them, you can read in more detail on our website in other articles.

STS "income" - 6%

The procedure for calculating the simplified system in this case is very simple; to calculate it, you need to take all the income received and multiply by the rate, which is 6%.

Example

Suppose you received an income of 1 million rubles, then the income will be calculated according to the following scheme:

Tax = Income * 6%,

In our case, 1,000,000 * 6% = 60,000 rubles.

Please note that expenses under the STS “income” are not taken into account in any way. Therefore, it should be used in the event that the costs are very difficult to confirm or their share is very small. The 6% system is mainly used by individual entrepreneurs who work without employees or have a small staff; due to simple accounting, you can do without accountants and not use accounting outsourcing.

STS "Income minus expenses" - 5-15%

This tax calculation system is more complex, and most likely it will be very difficult to do without a qualified accountant alone. However, the correct application of this system can save taxes and should be applied in the event that the LLC or individual entrepreneur can confirm the costs.

Attention! It is believed that this simplified taxation system is more profitable than 6% if it is at least 50% of income.

The tax rate, as a rule, is 15%, but it can be reduced in the regions to 5% and in the case of certain types of activities. The details of the reduced rate should be checked with your tax office.

Example

Let us also take an annual income of 1 million rubles, and take expenses in the amount of 650 thousand rubles, and calculate taxes at a rate of 15%.

Tax = (Income - expenses) * rate (5-15%)

In our case: (1,000,000 - 650,000) * 15% = 52,500

As you can see in this case, the amount of the tax will be less, but accounting is much more difficult. At the same time, not all expenses under the simplified taxation system, income minus expenses, are fashionable to take into account when calculating the tax, in more detail you can read about this taxation by clicking on the link.

Minimum tax and loss

Another nuance that this system has is the minimum tax. It is paid if the estimated tax is less than this amount or even zero, its rate is 1% of the amount of income, excluding expenses incurred (Tax Code of the Russian Federation, Article 346.18). So, if we take the example described by us, then the minimum tax will be 10,000 rubles. (1 million rubles * 1%), even if you have counted, for example, 8000 rubles for payment. or 0 rubles.

Even if your expenses were equal to income, which would essentially lead to a zero base in the calculation of tax, you still need to pay this 1%. There is no minimum tax when calculating “on income”. If, based on the results of the past tax period, the taxpayer incurred a loss, then this amount can be included in expenses in subsequent years, and, accordingly, the amount of tax can be reduced.

Reducing the simplified taxation system by the amount of insurance premiums

One of the positive aspects of the simplification is that the amount of tax can be reduced by the amount of insurance premiums transferred to the FIU. However, there are some peculiarities, both when choosing a system for calculating taxes, and in the presence of employees.

Simplified taxation system - individual entrepreneur according to the "Income" system without employees

As you know, an entrepreneur can work without hired employees, while he only pays a payment to the Pension Fund for himself, which is set by the government for each year. So in 2016 its value is 23,153.33 (PFR and MHIF). This payment allows you to reduce the amount of tax by its entire amount (by 100%). Thus, an individual entrepreneur may not even pay this tax at all.

Example

Ivanov V.V. over the past year earned 220,000 rubles, and Petrov A.A. earned 500,000 rubles, both paid the above payment for themselves in full, as a result, taxes for them are calculated as follows:

For Ivanov: Tax = 220,000 * 6% = 13,200, since the amount of payment to the Pension Fund for oneself is greater than the received value, so the total tax value will be zero.

For Petrov: Tax = 500,000 * 6% = 30,000, we deduct the payment for ourselves, we get that the amount of tax payable will be 30,000 - 23,153, 33 = 6,846, 67.

Simplified taxation system - individual entrepreneurs and LLCs according to the "Income" system with employees

This situation can arise both for an organization that simply cannot work without workers, and for an individual entrepreneur. In this case, taxes can be reduced by the amount of payments for employees, but not more than by 50%. In this case, it is paid in full, but is not taken into account when reducing.

Example 1

Petrov earned 700,000 rubles, and payments to the Pension Fund for employees amounted to 18,000 rubles. In this case, we get:

Tax = 700,000 * 6% = 42,000, since the amount of payments to the Pension Fund for employees does not exceed 50% of the amount received, then the STS can be completely reduced by it. The tax payable in this case will be equal to 24,000 (42,000 - 18,000).

Example 2

Suppose the same Ivanov (or LLC "Ivanov and K") earned 700,000, while in the Pension Fund he paid 60,000 rubles for employees.

Tax = 700,000 * 6% = 42,000 rubles, while it can reduce no more than 50% of taxes, in our case it is 21,000 than 21 thousand, that is, no more than 50%. As a result, the Tax payable will be 21,000 rubles (42,000 - 21,000).

STS "income minus expenses"

In this case, the presence or absence of employees does not matter. In this case, it is not the tax itself that decreases, but as in the examples considered above, but the tax base... Those. the amount of payments to the Pension Fund of the Russian Federation is included in the amount of expenses and the tax will be calculated from the difference at the applicable rate.

Example

So, if Petrov received income in the amount of 500,000 rubles, and the expenses were - rent 20,000 rubles, salary 60,000, payments to the Pension Fund for employees amounted to 18,000, for himself.

Tax payable = (500,000 - 20,000 - 60,000 - 18,000 - 23,153.33) * 15% = 378,846.76 * 15% = 56,827.

As you can see, the calculation principle is somewhat different.

Payment of 1% to the Pension Fund on income of more than 300,000 rubles

Please note that if an individual entrepreneur received income for the reporting period of more than 300 thousand rubles, then an additional 1% of the excess amount is paid to the pension fund (PFR). For example, if you received an income of 400,000 rubles, then you will need to pay additionally (400,000 - 300,000) * 1% = 1,000 rubles.

Important! In a letter dated December 7, 2015 under the number 03-11-09 / 71357, the Ministry of Finance explained that this payment will be equated to a mandatory fixed payment, so the STS can also be reduced by this amount. Do not confuse this amount with the minimum tax!

Reporting and payment of tax

This type of taxation implies the following reporting:

This type of taxation implies the following reporting:

- Declaration on the simplified tax system provides once a year, the deadline is until April 30 of the year, which follows the previous one.

- Entrepreneurs should be led, the abbreviated name is KUDiR. Since 2013, its certification with the Federal Tax Service is not required. But it should be laced, stitched and numbered in any case, but if zero reporting is provided, in some regions it is not required.

If an entrepreneur stops his activities under the simplified tax system, then he must submit a declaration according to the simplified tax system no later than the 25th day of the month following the one in which it stopped.

Payment of taxes

Although reporting is provided once a year, you will still have to keep records constantly, because payments under the simplified tax system are divided into 4 parts - 3 of them are advance and mandatory, like the 4th final payment for the year. At the same time, if you do not pay advance payments or pay correctly, then you may be charged with fines and penalties.

The due dates for payment of advances and tax are as follows:

- For the first quarter, the payment must be made by April 25th.

- For the second quarter, payment is due until July 25th.

- For the third quarter, payment is due until October 25th.

- Annual and final settlement is carried out no later than April 30 of the year that follows the reporting one. Those. for example, April 30, 2017 would be the 2016 tax deadline.

Responsibility for revealed violations

- If you are late or simply did not submit the tax return on time, the fine will be 5-30% based on the amount of tax that was required to be paid. In this case, the minimum fine is 1,000 rubles.

- If you did not pay taxes, then the penalties will be 20-40% based on the amounts that you did not pay.

- If payments are delayed, penalties are charged exactly as well as their incorrect calculation.

STS (simplified taxation system) is a special / special tax regime applied by legal entities in order to reduce the tax burden. This mode replaces the need to pay:

- VAT (excluding import);

- Income tax;

- Property tax;

- Personal income tax (for individual entrepreneurs).

Transition to simplified taxation system, restrictions

The transition to this type of taxation is voluntary. For the transition to the simplified tax system legal. individuals must submit a special notification form to the Federal Tax Service at the place of registration before the end of the calendar year (31.12). For newly registered organizations, a period of up to 30 days from the date of state registration is given to submit a notification. registration.

Art. 346.12NK RF provides for a number of restrictions for using the simplified tax system: (click to open)

- if the proceeds are more than 60 million rubles. based on the results of the tax period;

- if the average number of employees is more than 100;

- if the final price of depreciable fixed assets exceeds 100 million rubles;

- if the firm has branches;

- banks;

- pawnshops;

- investment funds;

- notaries;

- insurers, etc.

Tax Code provides for 2 options for applying the simplified tax system income 6% or income minus expenses. There is an unspoken rule: if the amount of expenses is more than 60% of the amount of income, it is better to go to the object of income minus expenses.

The declaration must be submitted once a year. But it is necessary to calculate and pay tax every quarter on an accrual basis.

STS calculation income minus expenses

The calculation of the simplified tax income minus expenses is carried out according to the formula

USN = (D - R) × Nst,

D - income;

Р - expenses;

Нst is the tax rate.

Let's consider each of these concepts.

Types of income accounted for in the simplified tax system

The income of the enterprise includes:

- Proceeds from the sale of finished products manufactured by the company;

- Revenue from the sale of goods;

- Proceeds from the sale of property;

As well as other incomes provided for in Art. 250 Tax Code

- Buyers' advance payments;

- Interest from loans provided by the company;

- Income from renting out property;

- The cost of property, work or services received free of charge;

- Amounts of fines, penalties received from counterparties on the basis of a court order;

- Other

All of the above incomes are accepted for accounting on a cash basis, that is, the date of recognition of the proceeds is the date of receipt of funds to the bank account or to the cash desk of the enterprise.

Types of expenses accounted for in the simplified tax system

In the context of accounting transactions, accounting for each action of the enterprise, including its expenses, is made in a continuous, continuous record. In tax accounting, Art. 346.16 the procedure for determining costs is clearly fixed. That is, not all costs incurred by the company can be taken into account in the costs when calculating the simplified taxation system.

Consider the main costs provided for by this article:

1 .. Expenses for payment of goods and materials for subsequent sale to suppliers;

These expenses are included in the ledger upon the sale of goods and materials, that is, on a cash basis. Here 2 conditions must be met: the goods must be sold to the buyer and paid to the seller.

An example of calculating the simplified taxation system (income minus expenses)

Platan LLC received 2 batches of the same powder from the supplier. The price of powder in 2 lots has increased.

| N batch | date | Quantity | Price | Amount, rub. | Prepayment,% | Payment amount, rub. |

| 1 | 15.02.2016 | 300 | 60 | 18 000 | 50 | 6 000 |

| 2 | 05.03.2016 | 500 | 70 | 35 000 | 50 | 17 500 |

12.03.2016 sold 750 pcs. powder for 60,000 rubles, payment was made on the same day. The balance of 1 batch was transferred to the seller on 03/15/2016 in the amount of 6,000 rubles.

Total: as of March 31, 2016, the balance in the warehouse is 50 pcs. powder at a purchase price of 70 rubles, i.e. in the amount of 3,500 rubles;

Only paid goods can be taken into account. 1 batch was paid in full, i.e. RUB 18,000 for 300 pcs. Out of 2 lots, only 250 were paid. (500 × 50%) in the amount of 17,500 rubles.

Calculation of tax for 1 sq. 2016 will be the following:

(60,000 - 35,500) × 15% = 3 675 rubles. must be transferred to the budget.

But what if the goods are sold by a retail store with a wide range of products? In such a situation, it is worth using the formula proposed by the Ministry of Finance in a letter dated April 28, 2006 N 03-11-04 / 2/94. This document explains the procedure for writing off the costs of purchasing goods and materials and refers to the transitional 2006. But the formulas can be used today.

2 .. Expenses for the purchase of raw materials and inventories for production.

To include these costs in the ledger, there is no need to wait until the raw materials go through the processing process. In this case, the amount of costs for materials is included in expenses as the funds are transferred.

3 .. Associated costs for the purchase of goods and materials;

According to PBU 5/01, additional costs aimed at purchasing inventories increase their cost estimate. But in tax accounting, such costs must be written off in one of the following ways (clause 2 of article 346.17 of the Tax Code of the Russian Federation):

- average cost;

- FIFO (first came - first left);

- unit cost of goods and materials.

Important! The LIFO method has been excluded from 01.01.2015 from the code by Federal Law No. 81-FZ of 20.04.2014.

4 .. Input VAT;

The amount of input VAT is written off to the costs upon the sale of goods and materials (Letter of the Ministry of Finance of the Russian Federation dated February 17, 2014, No. 03-11-09 / 6275). At the same time, in the accounting book, the amount of VAT is accounted for in a separate column (Letters of the Ministry of Finance dated 02.12.2009 N 03-11-06 / 2/256, dated 18.01.2010 N 03-11-11 / 03).

Such costs can be taken into account in the amount of no more than 1% of the sales turnover (subparagraph 20 of paragraph 1 of article 346.16, paragraph 4 of article 264 of the Tax Code of the Russian Federation)

6 .. Expenses for the purchase of fixed assets;

To accept the OS for accounting, they must be paid for and put into operation. Costs can be posted on the date of the last transaction. The write-off takes place in equal installments within 12 months.

7 .. Costs of legal, accounting services;

8 .. Stationery Goods;

9 .. Remuneration of employees;

It is taken into account on the day of the actual payment of wages

10 .. Taxes and fees;

All costs must be economically justified. That is, the auditors need to explain that these costs were necessary for the effective operation of the firm.

To confirm expenses, you must have at least 2 primary documents: (click to open)

- confirming the fact of households. activities (sales receipt, invoice, certificate of completion);

- confirming the fact of payment (cash register check for cash payments or bank statement - for non-cash payments).

These requirements are provided for by Art. 252 of the Tax Code of the Russian Federation and in case of non-observance, the tax authorities can exclude the amount of costs from the taxable base and charge an additional simplified tax, and in addition to the tax and the sanctions provided for by Article 122 of the Tax Code of the Russian Federation.

Tax rate according to the simplified tax system

To calculate the tax, a tax rate of 15% is provided. But this indicator can be differentiated by regional authorities and take values from 5%. And from 2017 to 2021, local authorities will be able to reduce the rate to 3%.

In addition, for newly registered taxpayers - individual entrepreneurs operating in the social, scientific or industrial spheres, the regional authorities can set a rate of 0% for a period of 2 years. In this case, the minimum tax also does not need to be paid.

The regions are allowed to reduce the rate in order to attract investment to the territory of the subject and revise it annually.

You can find out the effective rate in force in the region of interest by contacting the Federal Tax Service.

Important! The differentiated tax rate does not need to be confirmed by any documents, since this is not a benefit (letter of the Ministry of Finance dated October 21, 2013 N 03-11-11 / 43791).

Calculation of the simplified tax system (income minus expenses) for example

The tax calculation must be made on a quarterly cumulative basis, that is, for 1 quarter, half a year, 9 months and at the end of the year, it is necessary to submit a declaration to the Federal Tax Service with an appendix of the income and expense book.

Tax must be paid every quarter. Let's look at an example.

The cash desk and the settlement account of Millennium LLC received for the goods sold and the documented expenses provided for by Art. 346.16 of the Tax Code of the Russian Federation.

| date | Amount for goods sold | The amount of confirmed expenses |

| 1 sq. 2015 | RUB 475 870 | RUB 453,331 |

| 2 sq. 2015 | RUB 553 467 | RUB 534 631 |

| 3 sq. 2015 | RUB 637,570 | RUB 589,335 |

| 4 sq. 2015 | RUB 533 654 | RUB 438,733 |

| Total: | RUB 2,200,561 | RUB 2,016,030 |

For 1 sq. the company needs to transfer 3 380.85 rubles. ((475 870 - 453 331) × 15%)

For Q2 - 2 825.40 rubles ((475 870 + 553 467 - 453 331 - 534 631) × 15%) - 3 380.85)

For 3 sq. - RUB 7,235.25 ((475 870 + 553 467 + 637 570 –453 331 - 534 631 - 589 335) × 15%) - 3380.85 - 2825.40)

For the year 14 238, 15 rubles. ((2,200,561 - 2,016,030) × 15%) - 3,380.85 - 2,825.40 -7,235.25).

The minimum level of tax under the simplified tax system for the regime of income minus expenses

If the calculated tax amount is less than 1% of the amount of income received, Art. 346.18 of the Tax Code of the Russian Federation obliges the taxpayer to pay the minimum tax.

To calculate it, you must use the formula:

Tax = Amount of revenue × 1%

It is necessary to calculate the amount of the minimum tax based on the results of the year.

Example of calculating the minimum tax level

The firm LLC "Alpha" for 2015 received income in the amount of 2 250 355 rubles. Consumption - 2 230 310 rubles.

Tax amount (2,250,355 - 2,230,310) × 15% = 3,006.75 rubles.

The amount of the minimum tax is 2,250,355 × 1% = 22,503.55 rubles.

That is, the company LLC "Alpha" must transfer 22 503, 55 rubles to the budget. at the end of the year.

The STS income minus expenses is one of the most attractive tax regimes for Russian businessmen. However, there are frequent cases of disputable situations with tax authorities. Therefore, when calculating the tax, it is important to include in expenses only economically justified and confirmed by at least 2 correctly completed documents costs, which are provided for in Art. 346.16 of the Tax Code of the Russian Federation,

The simplified taxation system is popular because it is focused on small businesses and allows you to pay only one tax instead of several taxes - the tax under the simplified tax system (clauses 2, 3, article 346.11 of the Tax Code of the Russian Federation).

There is not much time left before the submission of the declaration under the simplified taxation system: this year, organizations need to report by April 2, and individual entrepreneurs - by May 3.

Restrictions on the use of the simplified tax system

Tax payers under the simplified taxation system are organizations and individual entrepreneurs who have switched to this special regime and apply it in the manner prescribed by Ch. 26.2 of the Tax Code of the Russian Federation (clause 1 of Article 346.12 of the Tax Code of the Russian Federation).

Not every organization and not every entrepreneur can apply the "simplified" code. Articles 346.12 and 346.13 of the Tax Code of the Russian Federation provide for a number of restrictions.

Some of them concern only organizations (for example, the ban on the use of the simplified tax system in the presence of branches), some are common for both legal entities and entrepreneurs.

TABLE: "Terms of use of the simplified tax system"

| The organization | SP |

| Limit size income on the simplified tax system in 2018 - 150 million rubles. If the income limit is exceeded, you must return to the DOS (clause 4 of article 346.13 of the Tax Code of the Russian Federation) | |

| To switch from DOS to USN from 2018, income for 9 months of 2017 must be no more than 112.5 million rubles. (Clause 2 of Article 346.12 of the Tax Code of the Russian Federation) | For individual entrepreneurs wishing to switch to the "simplified" system, restrictions on the amount of income, paragraph 2 of Art. 346.12 of the Tax Code of the Russian Federation does not provide for |

| The average number of employees is no more than 100 people (subparagraph 15 of paragraph 3 of article 346.12 of the Tax Code of the Russian Federation) | |

| Accounting residual value of fixed assets - maximum 150 million rubles (subparagraph 16 of paragraph 3 of article 346.12 of the Tax Code of the Russian Federation) | In relation to individual entrepreneurs, restrictions are not established by this rule (subparagraph 16 of paragraph 3 of article 346.12 of the Tax Code of the Russian Federation) |

| The maximum share of other organizations in the authorized capital is 25 percent (subparagraph 14 of paragraph 3 of article 346.12 of the Tax Code of the Russian Federation) | |

| Absence of branches (subparagraph 1 of paragraph 3 of article 346.12 of the Tax Code of the Russian Federation) | |

The simplified taxation system cannot be applied to budgetary and state institutions, banks, pawnshops and some other organizations.

Tax and reporting periods under the simplified tax system

For taxpayers applying the simplified tax system, the tax period is a calendar year, and the reporting periods are the first quarter, six months and 9 months of the calendar year (Article 346.19 of the Tax Code of the Russian Federation).

The tax period is the period after which the tax base is determined and the amount of tax payable to the budget is calculated (clause 1 of article 55 of the Tax Code of the Russian Federation). And according to the results of the reporting periods, subtotals are summed up, advance tax payments are paid.

USN tax rates

The rates of the simplified taxation system are determined by the provisions of Art. 346.20 of the Tax Code of the Russian Federation.1. The sizes of the general tax rates under the simplified taxation system for each of the objects of taxation (subparagraphs 1, 2 of article 346.20 of the Tax Code of the Russian Federation) are given in the table.

2. The possibility for all constituent entities of the Russian Federation to be established by the relevant laws:

- the sizes of differentiated tax rates in the range from 5 to 15 percent in relation to the object of taxation "Income minus expenses" depending on the category of taxpayers (clause 2 of article 346.20 of the Tax Code of the Russian Federation);

- tax rate of 0 percent for individual entrepreneurs registered for the first time after the entry into force of the relevant laws of the constituent entities of the Russian Federation and carrying out entrepreneurial activity in the production, social and (or) scientific sphere (clause 4 of article 346.20 of the Tax Code of the Russian Federation).

Form for filling out a declaration on the simplified tax system for organizations and individual entrepreneurs

The declaration under the simplified taxation system is handed over only at the end of the year. There is no quarterly reporting.

The form, the procedure for filling out, as well as the format for submitting in electronic form the tax declaration for the tax payable under the simplified tax system, approved by Order of the Federal Tax Service of the Russian Federation dated February 26, 2016 No. ММВ-7-3 / [email protected]

In the form, it is possible to reflect in the declaration the amount of the trade tax, which reduces the amount of the calculated tax under the simplified tax system, as well as the amounts of tax calculated using the rate of 0 percent in accordance with paragraph 4 of Art. 346.20 of the Tax Code of the Russian Federation.

To check the correctness of filling out the declaration under the STS, you can use the control ratios of the indicators of the tax declaration for the tax paid in connection with the use of the STS (sent by the letter of the Federal Tax Service of the Russian Federation of 05/30/2016 No. SD-4-3 / [email protected]).

The procedure for filling out the declaration for the simplified tax system "Income minus expenses" for 2017

What is required to be filled in:

- title page;

- sect. 2.2;

- sect. 1.2.

Section 3 is completed only by non-profit organizations.

The rest of the sections are for the STS "Income".

In section 2.2, lines 210-223 reflect income and expenses from the ledger of income and expenses. And in lines 240-243 - the difference between them, that is, the tax base. If in some periods income is less than expenses, the tax base is not shown, dashes are put. Losses are reflected in lines 250-253.

Line 230 is completed only if the previous year's loss is carried forward.

In lines 270-280 advance payments and tax are calculated according to the formulas specified in the declaration.

In section 1.2, only 5 lines are filled in. In line 010, OKTMO is put - you can find it on the website of the Federal Tax Service of the Russian Federation.

Lines 020, 040, 070 show advance payments paid for the first quarter, six months and 9 months. If at the end of the six months or 9 months there was an amount to be reduced, instead of lines 040 or 070, lines 050 or 080 are filled in.

Then one of three lines is filled in: 100, 110 or 120. If, at the end of the year, ordinary tax must be paid, its amount is indicated in line 100, if the minimum - in line 120. Line 110 is filled in if the calculated tax for the year is normal (line 273 section 2.2) or minimum (line 280 of section 2.2) - turned out to be less advance payments. It indicates the difference between tax and advance payments, which can be returned or offset.

Example. Filling out the declaration under the simplified tax system with the object "Income minus expenses" for 2017

In 2017, the address of the organization did not change, the tax base for losses from previous years did not decrease.

The minimum tax for 2017 is 18,000 rubles (1,800,000 rubles x 1 percent).

The amount of tax for the year is more than the minimum tax (139,500 rubles more than 18,000 rubles), which means that tax must be paid to the budget, calculated in accordance with the general procedure.

Advance payments and tax for 2017 are like this.

For the first quarter - 78,000 rubles.

For half a year - 12,750 rubles (90,750 rubles - 78,000 rubles).

For 9 months - 13 800 rubles (104 550 rubles - 90 750 rubles).

For the year - 34,950 rubles (139,500 rubles - 104,550 rubles).

Sections 1.2 and 2.2 of the declaration are completed as follows.

The procedure for filling out the declaration for the simplified tax system "Income" for 2017

With the object of taxation "Income" you need to fill in:

- title page;

- section 2.1.1;

- See section 1.1.

Section 3 is for non-profit organizations and section 2.1.2 is for trade tax payers.

The rest of the sections are needed for the STS "Income minus expenses".

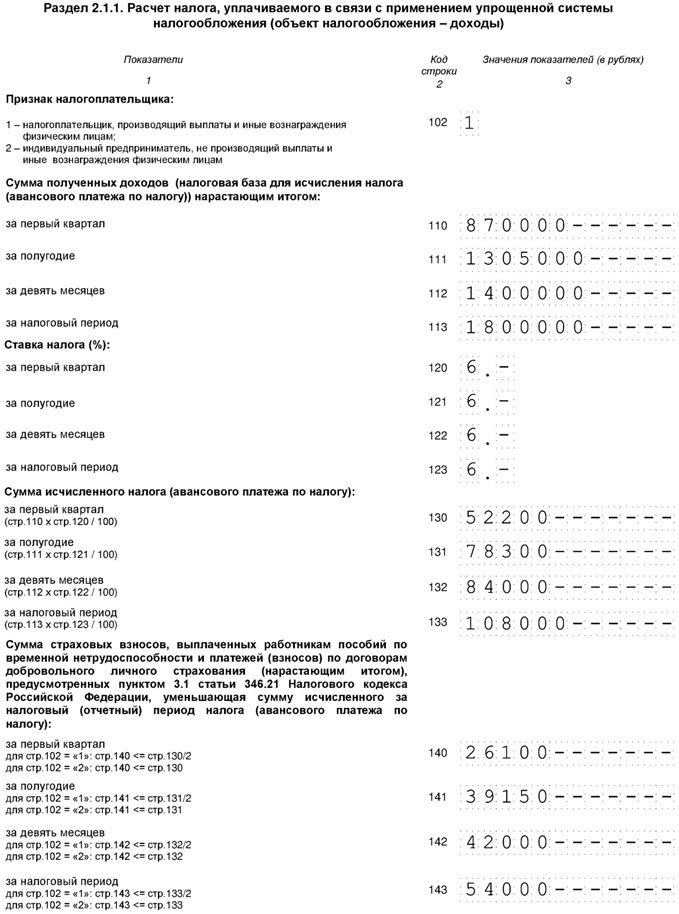

In section 2.1.1 on line 102 the sign "1" is put.

Lines 110-113 indicate the income for the first quarter, six months, 9 months and a year on an accrual basis from the beginning of the year, in lines 130-133 - the advance payments and tax calculated from them for the year.

Lines 140-143 reflect the amount of contributions and benefits that reduce tax.

Lines 020, 040, 070 indicate advance payments to be paid for the I quarter, half a year and 9 months. Line 100 - tax payable for the year.

If the simplified tax system is applied with the object of taxation "Income", the "simplified" tax must be paid on the entire amount of income (clause 1 of article 346.18 of the Tax Code of the Russian Federation). In this case, the expenses incurred are not taken into account when calculating the tax base, and the taxpayer is not obliged to document them (letters of the Ministry of Finance of the Russian Federation dated 06.16.2010 No. 03-11-11 / 169, dated 20.10.2009 No. 03-11-09 / 353).

An organization or individual entrepreneur has the right to reduce the amount of the calculated "simplified" tax (advance payments) by payment costs (clause 3.1 of article 346.21 of the Tax Code of the Russian Federation):

- insurance contributions for compulsory pension insurance;

- insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity;

- insurance premiums for compulsory health insurance;

- insurance contributions for compulsory social insurance against industrial accidents and occupational diseases;

- benefits for temporary disability.

Example. Filling in the declaration under the simplified tax system with the object "Income" for 2017

In 2017, the address of the organization did not change and the trade fee was not paid.

To determine the advance payment payable at the end of the reporting period, there is a formula:

AP = APResch - NV - APisch,

where APResch is an advance payment attributable to the tax base, determined from the beginning of the year to the end of the reporting period for which the calculation is made;

НВ - tax deduction in the amount of contributions paid for compulsory social insurance and benefits paid to employees for temporary incapacity for work;

APisch - the amount of advance payments calculated (payable) based on the results of previous reporting periods (in the current tax period).

Thus, the advance payments and tax payable for 2017 will be as follows.

For the first quarter - 26,100 rubles (52,200 rubles - 26,100 rubles).

For half a year - 13,050 rubles (78,300 rubles - 39,150 rubles - 26,100 rubles).

For 9 months - 2,850 rubles (84,000 rubles - 42,000 rubles - 26,100 rubles - 13,050 rubles).

For the year - 12,000 rubles (108,000 rubles - 54,000 rubles - 26,100 rubles - 13,050 rubles - 2,850 rubles).

The procedure for filling out the declaration on the simplified tax system for individual entrepreneurs for 2017

An individual entrepreneur pays (letters from the Ministry of Finance of the Russian Federation dated 16.11.2017 No. 03-15-05 / 75662, dated 04.09.2017 No. 03-15-05 / 56580):

- a fixed payment for oneself, which does not depend on the amount of income;

- an additional contribution for oneself from income over 300,000 rubles per year;

- contributions for employees.

The fixed payment for 2018 is 32,385 rubles. It includes a contribution for the OPS - 26,545 rubles and a contribution for compulsory medical insurance - 5,840 rubles (subparagraphs 1, 2, paragraph 1 of article 430 of the Tax Code of the Russian Federation). The deadline for payment of the fixed payment for 2018 is no later than 09.01.2019. It can be paid in installments throughout the year or in a lump sum. Individual entrepreneur on the simplified tax system “Income minus expenses” does not separately reduce the tax on contributions. All contributions paid both for oneself and for the employee are included in expenses (subparagraph 7 of paragraph 1 of article 346.16 of the Tax Code of the Russian Federation). If the individual entrepreneur has chosen the object "Income minus expenses", then the following is filled in:

- title page;

- sect. 1.2;

- sect. 2.2.

The rules for filling them out are the same as for organizations.

If the entrepreneur has chosen the object "Income", then the following is filled in:

- title page;

- sect. 1.1;

- sect. 2.1.1.

An individual entrepreneur on the STS "Income", who has employees, reduces the tax on contributions both for himself and for employees (letter of the Ministry of Finance of the Russian Federation dated February 10, 2017 No. 03-11-11 / 7567). But the total amount of the reduction cannot be more than 50 percent of the calculated tax (subparagraph 3 of paragraph 3.1 of article 346.21 of the Tax Code of the Russian Federation). The tax is reduced in the same manner as for organizations.

Individual entrepreneur on the simplified tax system "Income" without employees reduces the tax on contributions for themselves paid from the beginning of the year. For what period they are charged, it does not matter (letters of the Ministry of Finance of the Russian Federation dated 01.03.2017 No. 03-11-11 / 11487, dated 27.01.2017 No. 03-11-11 / 4232). For example, in January 2018, an individual entrepreneur paid a fixed payment for 2017. The tax for 2017 cannot be reduced on it, but the advance payment for the first quarter of 2018 can be reduced. The tax can be reduced by the full amount of contributions. If the contributions are greater than tax, the tax is considered zero.

Therefore, the filling rules are slightly different if the individual entrepreneur does not have employees:

- in line 102 sec. 2.1.1 you must specify code 2;

- and in lines 140-143 - insurance premiums for oneself, on which the tax has been reduced.

Example. Filling in the declaration under the STS "Income" for individual entrepreneurs without employees.

In 2017, the income of individual entrepreneurs amounted to 150,000 rubles for each quarter. In March 2017, he paid an additional fee for the OPS for 2016 - 1,800 rubles, in December 2017 - a fixed payment of 27,990 rubles.

I quarter

An advance payment of 9,000 rubles (150,000 rubles x 6 percent) is reduced by an additional payment for GPT. Advance payment payable - 7,200 rubles (9,000 rubles - 1,800 rubles).

Half a year

The advance payment - 18,000 rubles (150,000 rubles + 150,000 rubles) x 6 percent) is reduced by an additional payment for GPT and an advance payment for the previous period. Advance payment payable - 9,000 rubles (18,000 rubles - 1,800 rubles - 7,200 rubles).

9 months

An advance payment of 27,000 rubles (150,000 rubles + 150,000 rubles + 150,000 rubles) x 6 percent) is reduced by an additional contribution for GPT and advance payments for previous periods. Advance payment payable - 9,000 rubles (27,000 rubles - 1,800 rubles - 7,200 rubles - 9,000 rubles).

The tax calculated at the end of the year is 36,000 rubles (150,000 rubles + 150,000 rubles + 150,000 rubles + 150,000 rubles) x 6 percent) is reduced by an additional contribution for GPT - 1,800 rubles, a fixed payment - RUB 27,990 and advance payments for previous periods - RUB 25,200 (RUB 7,200 + RUB 9,000 + RUB 9,000). The calculated tax amount for the year is 36,000 rubles less than the amount to be reduced - 54,990 rubles (1,800 rubles + 27,990 rubles + 25,200 rubles), so there is no need to pay tax.

Minimum tax for STS

For taxpayers who have chosen the object of taxation “Income minus expenses”, the legislator introduced such a concept as the minimum tax (clause 6 of article 346.18 of the Tax Code of the Russian Federation).

The minimum tax is the mandatory minimum amount of the “simplified” tax.

Only individual entrepreneurs are exempted from its payment, who are allowed to apply a rate of 0 percent on the basis of paragraph 4 of Art. 346.20 of the Tax Code of the Russian Federation (paragraph 2 of this clause).

The minimum tax rate is defined in par. 2 p. 6 art. 346.18 of the Tax Code of the Russian Federation and is 1 percent of income for the tax period. It is unchanged and is applied in the specified amount, even if the law of the subject of the Russian Federation establishes a reduced differentiated rate in accordance with paragraph 2 of Art. 346.20 of the Tax Code of the Russian Federation (see also the letter of the Ministry of Finance of the Russian Federation dated May 28, 2012 No. 03-11-06 / 2/71).

The taxpayer is obliged to pay the minimum tax if the amount of tax calculated by him for the tax period in accordance with the general procedure is less than the amount of the minimum tax. Such a rule is established in par. 3 p. 6 art. 346.18 of the Tax Code of the Russian Federation.

The minimum tax must be paid also when, at the end of the year, a loss is received and the amount of tax calculated in the general procedure is equal to zero (see, for example, letters of the Ministry of Finance of the Russian Federation dated 20.06.2011 No. 03-11-11 / 157, dated 01.04.2009 No. 03-11-09 / 121, Federal Tax Service of the Russian Federation dated July 14, 2010 No. ShS-37-3 / [email protected], UFNS in Moscow dated 09.12.2010 No. 16-15 / [email protected], Resolutions of the Federal Antimonopoly Service of the West Siberian District of 20.05.2008 No. F04-3006 / 2008 (5051-A45-27), FAS of the Central District of 22.01.2007 No. A08-2668 / 06-9).

The difference between the paid minimum tax and the amount of tax calculated according to the general procedure can be included in expenses in the following tax periods. Including this amount, you can increase the amount of losses that are carried forward in accordance with paragraph 7 of Art. 346.18 of the Tax Code of the Russian Federation. This is stated in par. 4 p. 6 art. 346.18 of the Tax Code of the Russian Federation (see also letters of the Ministry of Finance of the Russian Federation dated 20.06.2011 No. 03-11-11 / 157, dated 11.05.2011 No. 03-11-11 / 118, dated 08.10.2009 No. 03-11-09 / 342, dated 17.08.2009 No. 03-11-09 / 283, dated 01.04.2009 No. 03-11-09 / 121, Federal Tax Service of the Russian Federation dated 14.07.2010 No. ShS-37-3 / [email protected]).

For example: the amount of the minimum tax at the end of 2016 was 5,000 rubles, and the amount of tax calculated according to the general procedure is 4,500 rubles. The difference in the amount of RUB 500 (RUB 5,000 - RUB 4,500) can be charged to expenses in 2017 (and, if a loss occurs, reflected in losses).

This difference can be included in expenses (or increased by the amount of the loss) in any of the subsequent tax periods.

This conclusion follows from par. 4 p. 6 art. 346.18 of the Tax Code of the Russian Federation. The Ministry of Finance of the Russian Federation also agrees with him. At the same time, the department emphasizes that the difference between the amount of the minimum tax paid and the amount of tax calculated according to the general procedure for several previous periods may be included in expenses at a time (letters of the Ministry of Finance of the Russian Federation of January 18, 2013 No. 03-11-06 / 2/03, dated 07.09.2010 No. 03-11-06 / 3/125).

For example, when calculating a single tax based on the results of 2012, 2013, the organization formed a positive difference between the amount of the minimum tax paid and the amount of tax calculated in the general manner. The organization has the right to include it in expenses when calculating tax for 2014 or 2015 or another tax period following it.

The minimum tax amount is calculated for the tax period - a calendar year. This follows from par. 2 p. 6 art. 346.18 of the Tax Code of the Russian Federation.

Therefore, it is not necessary to calculate and pay the minimum tax for the first quarter, six months, 9 months.

The minimum tax is calculated as follows:

MN = NB x 1 percent,

where NB is the tax base calculated on an accrual basis from the beginning of the year to the end of the tax period. The tax base for the purpose of calculating the minimum tax is income determined in accordance with Art. 346.15 of the Tax Code of the Russian Federation. In the case of combining the simplified tax system with another tax regime, for example, with the patent taxation system, the amount of the minimum tax is calculated only on income received from "simplified" activities (letter of the Ministry of Finance of the Russian Federation dated 13.02.2013 No. 03-11-09 / 3758 (sent by letter of the Federal Tax Service RF dated 06.03.2013 No. ED-4-3 / [email protected])).

The minimum tax is paid in the same manner as the “simplified” tax.

An example of calculating the minimum tax.

The organization "Zima", which uses the simplified taxation system (object of taxation "Income minus expenses"), received income in the amount of 100,000 rubles for the tax period, and its expenses amounted to 95,000 rubles. That is, the tax base for the tax is 5,000 rubles (100,000 rubles - 95,000 rubles).

1. The amount of tax, based on the income received during the tax period and the expenses incurred, will amount to 750 rubles (5000 rubles x 15 percent).

2. The amount of the minimum tax: the income received during the tax period (without reducing them to expenses) is multiplied by 1 percent. The minimum tax will be 1,000 rubles (100,000 rubles x 1 percent).

3. We compare the amount of tax calculated in the general order and the amount of the minimum tax (750 rubles less than 1,000 rubles).

4. We pay to the budget the minimum tax in the amount of 1,000 rubles, since its amount exceeded the amount of tax calculated in accordance with the general procedure.

How to account for advance payments against the minimum tax.

Organizations or individual entrepreneurs applying the simplified tax system with the object "Income minus expenses", at the end of each reporting period, calculate the amount of the advance payment according to the rules of clause 4 of Art. 346.21 of the Tax Code of the Russian Federation. In this case, the previously calculated amounts of advance tax payments under the simplified taxation system are counted when calculating the amount of tax for the tax period (clause 5 of article 346.21 of the Tax Code of the Russian Federation).

If for the tax period the amount of the tax calculated in the general procedure is less than the calculated minimum tax, then the “simplified person” with the object of taxation “Income minus expenses” pays the minimum tax (clause 6 of article 346.18 of the Tax Code of the Russian Federation).

The provisions of Ch. 26.2 of the Tax Code of the Russian Federation does not directly provide for the right of the taxpayer to set off the advance tax payments paid by him under the simplified tax system against the payment of the minimum tax. However, such a right follows from the declaration form under the simplified tax system, which was approved by Order of the Federal Tax Service of the Russian Federation dated February 26, 2016 No. ММВ-7-3 / [email protected], since section 1.2 provides for line 120, which indicates the amount of the minimum tax payable for the tax period. At the same time, in clause 5.10 of the Procedure for filling out this declaration, approved by Order of the Federal Tax Service of the Russian Federation dated February 26, 2016 No. ММВ-7-3 / [email protected], it is provided that if the amount of the calculated tax for the tax period is less than the amount of the calculated minimum tax for this period, then the amount of the minimum tax payable for the tax period is indicated minus the amount of the calculated advance tax payments.

Zero declaration according to the simplified tax system

If, for any reason, taxpayers temporarily suspend their business activities and do not receive income, they do not need to charge and pay tax.

But the declaration must be submitted. The fact is that the obligation to submit a declaration does not depend on the results of entrepreneurial activity. This conclusion was confirmed by the Constitutional Court of the Russian Federation in the Ruling No. 499-О-О dated 17.06.2008.

In this regard, the question arises: what kind of declaration to submit - single (simplified) or zero?

It depends on the movement of funds in bank accounts (at the cash desk).

If money went through bank accounts (at the cash desk), you need to submit a regular tax return under the simplified tax system.

If, at the same time, there are no income and expenses, a declaration with zero indicators (zero declaration) is submitted.

Unified (simplified) declaration according to the simplified tax system

Taxpayers have the right to submit a single (simplified) declaration, subject to the following conditions (paragraphs 2-4, clause 2, article 80 of the Tax Code of the Russian Federation):

- there is no cash flow on their bank accounts and at the cash desk;

- they have no objects of taxation for one or more taxes.

This situation can arise if business is temporarily suspended, there is no income, and no expenses are incurred.

The simplified declaration form and the procedure for filling it out are approved by Order of the Ministry of Finance of the Russian Federation of July 10, 2007 No. 62n.

True, this reporting is inconvenient and is rarely used in practice.

What you should pay attention to.

- it is necessary to carefully control that there are no monetary transactions on bank accounts. Tracking this is quite laborious, especially those payments that the bank can write off automatically (for example, its commission for settlement and cash transactions). Meanwhile, in this case, it is impossible to submit a single (simplified) declaration. If, not knowing about the expense transaction, submit a simplified declaration instead of the usual one, then the tax authorities may be fined under Art. 119 of the Tax Code of the Russian Federation.

- according to clause 2 of Art. 80 of the Tax Code of the Russian Federation, a single (simplified) declaration is submitted quarterly: no later than the 20th day of the month following the expired quarter, half year, 9 months, calendar year.

At the same time, the Ministry of Finance of the Russian Federation expressed the opinion that it is possible to submit a single (simplified) declaration only at the end of the tax period, since Ch. 26.2 of the Tax Code of the Russian Federation does not provide for the obligation to file tax returns based on the results of reporting periods (letter dated 05.05.2017 No. 03-02-08 / 27798). This approach, in our opinion, may lead to claims by the tax authorities. Therefore, for clarification on the question of whether it is possible not to submit a single (simplified) declaration based on the results of the reporting periods, we recommend that you contact your tax authority. Note that a regular tax return is submitted only once a year (Article 346.23 of the Tax Code of the Russian Federation).

- it makes sense to submit a single (simplified) declaration if it replaces reporting on several taxes at once. But under the simplified tax system, it is unlikely that it will be possible to take advantage of such an advantage, since instead of the main taxes (on profit, personal income tax, VAT, property tax), organizations and entrepreneurs pay one “simplified” tax.

Therefore, if the entrepreneurial activity is temporarily not conducted and there is no income, then it is advisable to submit to the tax authorities a zero ordinary declaration for the simplified tax system.

Terms of submission of the declaration on the simplified tax system by organizations and individual entrepreneurs

The deadlines for submitting the declaration are established by Art. 346.23 of the Tax Code of the Russian Federation.Let's consider them in more detail.

TABLE: "Terms of delivery of the STS declaration"

If the last day of the term falls on a day recognized in accordance with the legislation of the Russian Federation as a day off and (or) a non-working holiday, then the declaration must be submitted no later than the next following working day (clause 7 of Article 6.1 of the Tax Code of the Russian Federation). This rule also applies if the deadline for filing the declaration is on Saturday, which is a working day in your office. In this case, the day of the expiration of the deadline for filing the declaration will also be considered the Monday following the weekend.

Terms of payment of tax and advance payments under the simplified tax system

TABLE: "Terms of payment of tax and advances under the simplified tax system"

| The organization | SP |

| Pay tax and advances on the simplified taxation system at the place of their location | Pay tax and advances on the simplified tax system at their place of residence |

Advance payments: are subject to transfer no later than the 25th day of the first month following the expired reporting period (clause 7 of article 346.21 of the Tax Code of the Russian Federation). In 2018:

|

|

STS-tax: no later than March 31 of the year following the expired tax period (clause 7 of article 346.21, clause 1 of clause 1 of article 346.23 of the Tax Code of the Russian Federation); for 2017 - no later than 02.04.2018 | STS-tax: no later than April 30 of the year following the expired tax period (clause 7 of article 346.21, clause 2 of clause 1 of article 346.23 of the Tax Code of the Russian Federation); for 2017 - no later than 03.05.2018 |

Upon termination of an activity in respect of which the simplified taxation system was applied, taxpayers must pay tax no later than the 25th day of the month following the month in which, according to the notification submitted to the tax authority, such activity ceased (clause 7 of article 346.21, clause . 2 article 346.23 of the Tax Code of the Russian Federation); |

|

In case of loss of the right to use the simplified taxation system, taxpayers must pay tax no later than the 25th day of the month following the quarter in which they lost this right (clause 7 of article 346.21, clause 3 of article 346.23 of the Tax Code of the Russian Federation). |

|

If the last day of the due date for the payment of the tax (advance payment) falls on a weekend and (or) a non-working holiday, the tax (advance payment) must be transferred no later than the next following working day (clause 7 of article 6.1 of the Tax Code of the Russian Federation).

Late transfer of tax (advance payment) entails the accrual of penalties in accordance with Art. 75 of the Tax Code of the Russian Federation (clause 2 of article 57, clause 3 of article 58 of the Tax Code of the Russian Federation).

Method of submitting a declaration according to the simplified tax system

Taxpayers have the right to choose how to submit a declaration under the simplified tax system: on paper or in electronic form (clause 3 of article 80 of the Tax Code of the Russian Federation).Tax declarations must be submitted exclusively in electronic form (paragraphs 2, 4, paragraph 3, article 80 of the Tax Code of the Russian Federation):

- taxpayers whose average number of employees for the previous calendar year exceeds 100 people;